Global ocean snapshot

Global container shipping market is soft but carriers are doing their bestto keep it tightly managed. Demand is slightly higher than last year overall but very uneven by trade. Carriers still are using blank sailings, Red Sea routing choices, and GRIs to try to hold rates above their floor, while port and inland congestion—not lack of space—remain the main service risks.

I. Top 5 ocean & air issues for shippers / BCOs / importers

- Soft demand, sharp lane differences – Volumes are up only a few percent, leaving Transpacific weak, Asia–Europe/Med & Intra-Asia firmer, and India and Southeast Asia as key swing origins.

- Overcapacity hidden by blank sailings – Newbuilds keep capacity high, while scrapping old vessels remains stagnant. Carriers continue using blank sailings to tighten real capacity trying to backstop their GRIs.

- November GRIs mixed results Transpacific has already given back the recent GRIs while Asia–Europe/Med have held firm. Intra-Asia also holds their GRIs well but Transatlantic kept part.

- Port and inland congestion pockets – North Europe hubs, parts of South China and Southeast Asia, Australia, and many North American rail ramps add days of delay even if vessels arrive on time.

- Airfreight tight out of Asia –Export volumes remain high, with limited air freighter and tight belly space pushing rates higher. Heavy equipment and electronics should keep volumes high into 2026.

II. Major ocean trade-lane updates

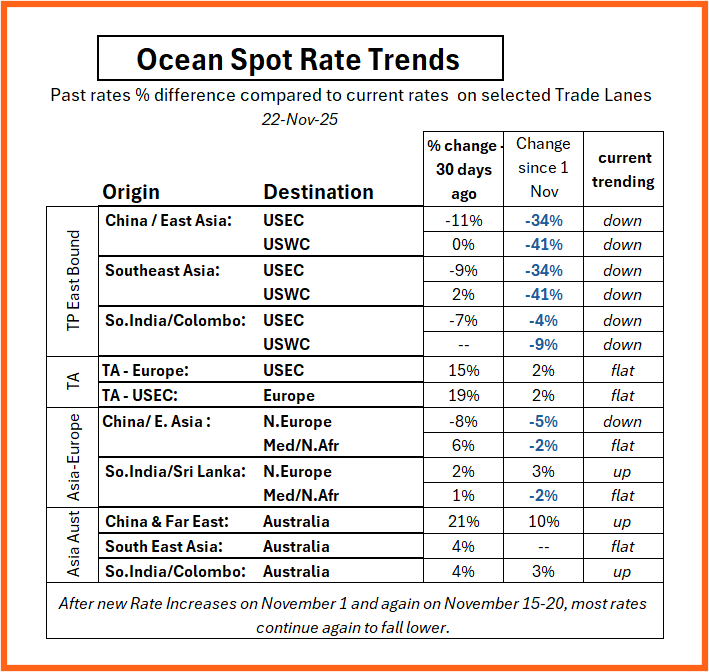

1. Far East / Southeast Asia → North America (USEC + USWC)

a. Current demand

Soft to stable overall. Imports for holiday sales are largely in place, so volumes are down from early Q4 peaks, with USEC holding better than USWC.

b. Capacity / supply

Good capacity available. Carriers continue with selective blank sailings (10-15%) as much as they can to try to hold last rate increases.

c. Spot rate level change

Broadly +10–25% versus early October after GRIs, but roughly flat or lower versus 1 November GRIs. USEC spots are slightly lower than contract and softer than USWC.

d. 2–3 month forecast

Market stays shipper-leaning unless a new restocking wave or policy shock bumps demand. Expect choppy, mostly sideways pricing with periodic GRIs that only partly stick.

2. Indian Subcontinent → North America (USEC + USWC)

a. Current demand

Modest, with US tariffs keeping a lid on some India flows, but diversification away from China supporting baseline volumes.

b. Capacity / supply

Generally open services and reasonable equipment at main load ports; no structural squeeze.

c. Spot rate level change

From a very low floor, roughly +30–50% versus early October as GRIs and surcharges come in, but November GRIs fail to hold and have mostly reverted or lower.

d. 2–3 month forecast

Floor continues to rise off the bottom, but this remains a buyer-friendly trade. Good window to lock in contracts while carriers are still fighting for volume.

3. Far East / Southeast Asia → Europe & Mediterranean

a. Current demand

Slightly higher, helped by gradual European restocking and firm Med demand compared to North Europe.

b. Capacity / supply

Nominal capacity is strong, but lack of Red Sea/Suez routing return and port congestion (Rotterdam, Antwerp, Hamburg, etc. and some South Med) keep space tighter than it ought to be.

c. Spot rate level change

Asia–North Europe and Asia–Med are together up roughly 15–30% versus early October, and up about 5–15% versus 1 November, with continuing increases added on.

d. 2–3 month forecast

This stays one of the more carrier-favored corridors. Expect continued GRI/FAK attempts and firm levels into contract season, especially if Red Sea risk and European port congestion continue. If Suez/Red Sea routings reopen in a big way, then capacity will boom and rates fall.

4. Indian Subcontinent → Europe & Mediterranean

a. Current demand

Steady, supported by more sourcing shifts into this region.

b. Capacity / supply

Plenty of services; recent FAK/GRI filings tighten the price floor rather than physical space.

c. Spot rate level change

New FAK levels imply roughly +30–50% versus early October and +10–20% versus 1 November, depending on lane and carrier, but absolute levels remain competitive versus China.

d. 2–3 month forecast

Expect a more “normal” market rather than a fire-sale. Still good value versus Far East origins, but less room for ultra-low spot deals than earlier in the year.

5. Asia → Australia & New Zealand

(Far East + Southeast Asia + ISC to ANZ)

a. Current demand

Strong and still in peak mode, driven by retail, e-commerce and general merch; Southeast Asia and India volumes are growing alongside North Asia.

b. Capacity / supply

This is one of the tightest regions: ships frequently sail very full, some calls are skipped, and transshipment via Singapore, Port Klang and Laem Chabang can add several days.

c. Spot rate level change

Across North Asia and Southeast Asia to Australia, GRIs and restorations have pushed levels as high as +35% versus early October and about +15% versus 1 November, with only small reductions so far.

d. 2–3 month forecast

Always “book early or roll” through at least Lunar New Year. Very limited downside near-term; risk is more on service reliability and space than rate collapse.

6. Transatlantic (Eastbound + Westbound)

a. Current demand

North America→Europe is steady to soft; Europe→North America is stable but unspectacular.

b. Capacity / supply

Ample capacity in both directions, with only modest blank sailings; no major structural constraints.

c. Spot rate level change

Overall flattish versus early October and 1 November, leaving this corridor near cycle lows compared with the big Asia trades.

d. 2–3 month forecast

Remains one of the most shipper-friendly regions. Good time to secure value contracts and service commitments while carriers are keen to hold volume.

7. Intra-Asia & other regional trades

a. Current demand

Healthy on China–ASEAN and intra-ASEAN routes, plus solid flows into the Middle East and parts of Africa.

b. Capacity / supply

Generally adequate, but local bunching and hub congestion (South China, Singapore, Port Klang) can tighten space quickly.

c. Spot rate level change

Intra-Asia indices show around +25% versus early October, including a sharp jump in early November, though absolute price levels remain low compared with long-haul trades.

d. 2–3 month forecast

Short-haul trades stay sensitive to operations rather than macro demand. Focus on port selection, transit-time consistency, and contingency routings more than chasing the very lowest rate.

III. Ocean Spot Rate Trend Analysis on selected specific lanes

IV. Port conditions – where delays add up

- Many major North America, continue with some moderate levels of congestion and delays (3-5 days) or intermodal rail terminal delays (2-4 days) including ports of the West Coast and the major East Coast ports.

- Congestion issues continue to impact North Europe hub ports.

- Also, with congestion delays are selected South China, Southeast Asia, and Eastern Australia ports.

V. Conclusion

Ocean and air markets look calm on the surface—rates far below the last crisis peaks and plenty of ships in the water—but operations are uneven, and blank sailings, routing changes, congestion, and tight air capacity can quickly turn a “cheap” move into a late or costly one.

To protect service and cost consider WOWL:

- An ITMS, origin through destination management service including centralizing your orders; your bookings & routings; in transit tracking; milestones, and handling exceptions all the way to the door delivery.

- WOWL runs control towers also that combine experienced logistics professionals with AI tools that scan options, flag risks, and suggest next-best actions.

We are built on the mix of seasoned experts with smart technology to give the best control over service, reliability, and cost in a market. This philosophy provides the rewards of preparation and still does the last-minute heroics.

AndyG@WOWL.io

Website: WOWL.io