Period covered: 20 March – 5 April 2026

Opening snapshot

The Iran conflict now reaches well past the Gulf. It is pressuring oil, bunker, jet fuel, insurance, schedules, and freight pricing. That matters not just for transport fuel. Oil and natural gas feed fertilizers, plastics, chemicals, packaging, and other core materials that move through global supply chains every day. When that base gets shaken, the impact spreads much wider than freight alone.

Ocean freight is firmer than late February. Air freight is tighter still. But neither move is really about strong global demand. The push is coming from conflict, rerouting, fuel cost, and weaker network efficiency.

Key market points

A. Demand

Demand is soft to stable overall. Asia is still doing most of the lifting. Europe remains weak. North America is mixed and still not showing the kind of strength that would explain this market by demand alone.

If fossil fuel prices stay high or increase higher, it will start impacting overall global demand as it impacts many more portions of every economy. Lower demand will impact the ocean markets for sure. Lower rates will happen but at the cost of less orders/ less demand for us all.

B. Capacity

There is still plenty of capacity on paper. In practice, it does not feel that way. Blank sailings, longer routings, trapped Gulf tonnage, and slower equipment turns are tightening the market more than the raw vessel count suggests.

C. Structural / routing issue

Our biggest concerns include the Red Sea and Hormuz disruption are still the main structural issues. They are stretching transit times, raising fuel burn, and keeping a firmer floor under rates than soft demand normally would.

D. Reliability

This is really an execution market now. Problems are showing up in schedule reliability, transshipment timing, inland movement, and equipment turns before they show up as one clean global congestion story.

*Ocean continues to be the most unreliable form of major transport even as it shows some incremental improvements. Mostly consider that the carriers and NVOCCs are not holding themselves responsible for the origin to destination portions of transport that they are offering to customers.

E. Contracting season

Carriers have gained some leverage back, not because they fully control the market, but because the market has become less predictable. When reliability gets harder to secure, pricing power improves. Tough time to negotiate agreements when the geopolitical side is upside down. Might be best to consider quarterly or half year agreements and renegotiate in December for January.

F. Contract vs. Spot

Spot is moving faster than contract. That is especially true in air, but it is also true in ocean. Shippers are seeing more tactical pricing and less comfort in longer-duration assumptions.

Note that most every year spot & contract rates change positions on which is higher or lower. But over the course of every year, contracts fare better overall for customers. Consider a 70/30 or 80/20 split between contracting and using spot/short term pricing. This gives you flexibility to take advantage of opportunities that pop up.

Other top issues

- Blank sailings are still active into April.

- Fuel and emergency surcharges are now part of normal planning.

- Fog continues to disrupt some China port operations.

- Singapore is still absorbing displaced pressure from Middle East disruption.

- North Europe remains exposed to vessel bunching and yard crowding.

- India lanes are tightening, especially where feeder and Gulf exposure matter.

- Ocean transit times remain stretched on key east-west trades.

- Air contracts are shortening as the market leans back toward spot.

- Trade policy keeps adding cost and planning noise.

- Reliability matters!

HORMUZ / RED SEA WATCH

Near term

Cape routing remains the practical answer for many services. Suez relief is delayed again. Fuel, insurance, and schedule pressure stay high.

Transition risk

Even if conditions improve, the shift back will not be clean. Networks can get messier before they get better.

2026 impact

This keeps a firmer floor under ocean pricing and a higher volatility premium in air. Overcapacity still exists, but disruption is delaying when it fully matters.

Caution

If conflict cools, rates could soften quickly. If it spreads, fuel and routing costs could outrun weak demand.

Trade-lane snapshots

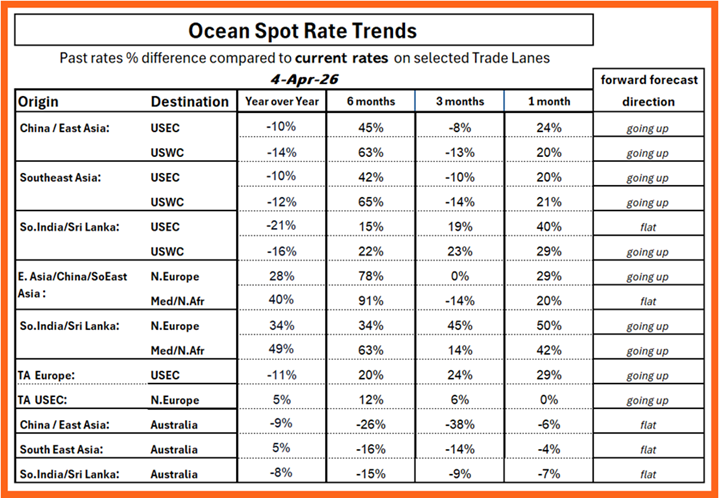

Transpacific | East & Southeast Asia -> North America West Coast

Better than February. Firmer than one month ago. Still below year-ago. Managed, not booming.

Transpacific | East & Southeast Asia -> North America East & Gulf

Demand improved some. Capacity is still managed. Rates are up. Reliability remains the bigger issue.

Asia -> North Europe & Mediterranean

Europe remains one of the firmer trades. North Europe looks supported. Med feels firm, but closer to steady than still climbing.

Indian Subcontinent -> North America & Europe

Still one of the tightest pressure points. Europe and USWC lanes lean up. USEC still looks elevated, but closer to flat than another jump higher.

Transatlantic | Europe <-> USEC

Still the calmest major trade. Slightly firm underneath, but stable.

Australia / Oceania

Still one of the softer groups. Flat to soft remains the better read.

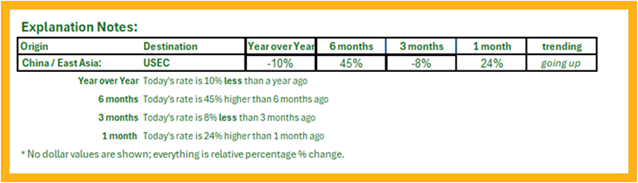

Ocean Rate Trends

Port & gateway watchlist for congestion/delay

Far East & Southeast Asia: Shanghai, Ningbo, Qingdao, Singapore

India & Middle East: Nhava Sheva, Mundra, Gulf routing sensitivity

North Europe: Antwerp, Rotterdam, Hamburg, inland Europe

Global Air Freight — quick view

Air remains the quicker-moving part of this market. Capacity is still constrained by Gulf disruption and rerouting. Demand is mixed, but strong enough on premium lanes to keep pressure on space and pricing. Near term, air stays more volatile than ocean.

Trade / compliance note

Importers who paid duties under IEEPA may be eligible for refunds after the Supreme Court ruling that the use of IEEPA had been extended beyond where it should have applied. At the same time, expect the White House to move quickly with a replacement tariff structure. A 15% duty has been announced, but the final details are still not settled. For now, importers should focus on recovering duties already paid under IEEPA while preparing for a new cost structure ahead.

Conclusion

For the next 4–6 weeks, book earlier where timing matters. Protect flexibility. This is a Best Practice to follow. Read fuel and surcharge language harder than base rates.

The bigger point is this: the market is not just reacting to one war. It is reacting to a world that is unsettled and could get worse before it gets better.

Freedom of navigation is under more strain. Chokepoints matter more. Politics is reaching deeper into freight. Overcapacity is still there, yes, but geopolitics is deciding when it matters.

WOWL helps shippers see that shift early and act before disruption lands in their freight.

#GlobalLogistics #OceanFreight #AirFreight #SupplyChain #ContainerShipping #TradeLanes #FreightMarket #WOWL #OriginManagement #POmgmt

Andy Gillespie

AndyG@WOWL.io

WOWL.io

Newsletter free subscription at WOWL.io